Get all the support related to select here. Start with finding your query.

Select is a free platform that helps you compare brokers and credit cards with ease. It offers detailed reviews, side-by-side comparisons, and helpful metrics so that investors and credit card users can make informed decisions.

You’ll also find unbiased articles, news updates, and feature breakdowns to stay on top of the investing and personal finance world. Whether you're exploring brokers or credit cards, Select helps you understand and evaluate your options confidently.

Step 1- Visit Select by Finology

Step 2- Click on ‘Find’

Step 3- Use quick 30 seconds wizard

Step 4- Answer 8 simple Yes/No type questions

Hurray! You now have a broker that matches your needs.

A 3-in-1 account is a bundled setup that links your bank account, Demat account, and trading account—making transactions seamless, faster, and more convenient.

With all three accounts connected, you can easily transfer funds, hold securities, and execute trades without the hassle of managing them separately.

Call and trade charges are fees that apply when you place an order directly through a dealing desk, instead of executing it online.

Margin refers to the money borrowed from a brokerage firm to leverage an investment. It’s the difference between the total value of securities in your account and the loan amount from the brokerage.

Buying on margin is essentially borrowing money to purchase securities. You pay a percentage (the margin) of the total cost, while the rest is financed by the broker.

Step 1- Kindly visit the Compare section.

Step 2- You can choose the brokers from the dropdown menu and compare Broker 1, Broker 2, and Broker 3.

Step 3- After choosing your brokers, you can click on “Start Comparing Now”.

Voila! You are ready to compare the features of your broker.

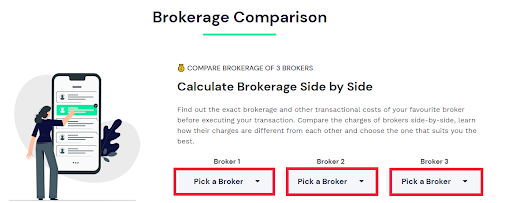

Step 1: Visit “Compare” section.

Step 2: Kindly choose the broker in the Broker 1, Broker 2, and Broker 3 column.

Step 3: After choosing the brokers, click on ‘Start Comparing Now’.

/content-assets/dfe20531fd1b4fc9a2443d03584841a4.png)

Step 4: You can enter the details as per your transaction, and click on the “Calculate" button.

/content-assets/fcbf0c91c4ea4e8ba61d7c584db1b3f2.png)

Yayyyyyy! Your charges comparision is ready.

The charges for opening a Demat account may vary for different brokers. For your help, we have the "Broker" section which will help you with the detailed charges of all the brokers.

We are well aware of your requirements and hence, we already have it ready for you. For the detailed Demat account opening guide, kindly Click here

There’s a common misconception that minors can’t invest in the stock market, but that’s not the case! There’s no age limit for investing. Minors can open a Demat account with the help of a guardian. Once the required documents are provided by the guardian, the account can be opened in the minor’s name. So, there’s no specific maximum or minimum age for opening a Demat account.

In order to know the process of opening a Demat account, you can refer to our step by step Demat account opening guide from here.

Please note that the document requirements vary from broker to broker. To know more about the detailed requirements and procedure, visit the ‘Account Opening’ section listed with each broker on Select.

No need to worry! You have to simply log in using the same credentials as earlier. It will automatically start the procedure from where you left.

Typically, the Demat account opening process takes around 48 to 72 hours. However, this timeline can vary depending on the stockbroker you choose and the speed at which they process the account opening.

It usually takes 48 to 72 hours to open a Demat account. But this may vary based on the chosen stock broker and their Demat account opening process. You can wait for the prescribed time and check your mailbox. Do not forget to check the spam folders as well.

If you still do not receive the confirmation, kindly contact your broker to know the status of your account.

Currently, in India, an NRI can open a Demat account only through an offline process. The procedure for account opening varies for different brokers. It would be best to connect with your preferred broker to know the detailed procedure and avoid any grievances.

At present, we do not offer a non-individual account opening process on Select. The account opening process for a non-individual is completely offline. So, it would be advisable to contact the broker for a detailed procedure.

Closing a Demat account usually requires downloading the closure form and filling it in. It is an offline process.

For a detailed step-by-step process and guidance, you may reach out to your broker or visit their respective website.

A credit card is a financial instrument provided by banks and even NBFCs to their customers. Credit cards allow their users to withdraw more money than is available in their accounts in the form of short term loan.

A credit card works by allowing users to make purchases at various locations using a type of short term loan. The credit card essentially makes the provider bank pay on behalf of the user and thus, needs to be paid back within the due date. Some credit cards also allow cash withdrawals, but care needs to be taken as these withdrawals are usually charged at a much higher rate.

Various providers have different processes for credit card applications. Certain documents like proof of identity, address and income are necessary by providers. These documents need to be submitted and the provider’s steps need to be followed to get a credit card.

For more detailed information on specific cards, find your card on select.finology.in and follow the process mentioned with your card of choice.

Credit cards give users access to short term credit that can help them improve their lifestyle by not having to wait for purchases. Credit cards also allow their users to build their credit score if they repay their dues on time.

However, care must be taken to not use credit cards in excess as failure to repay credit card due may lead to hefty interest charges and declining credit score as well.

Credit limit is the amount of borrowing a specific card will provide its user. This limit is set based on the user’s income, their credit score and credit history.

It is advised to not always use one’s credit card to its specified limit, just because the amount is accessible.

APR stands for Annual Percentage Rate and is the annual rate of interest levied on outstanding balance of your credit card.

Minimum payment is the least amount a credit card holder has to pay before the due date to avoid incurring interest on the outstanding balance.

Missing credit card payments is never a good idea. If you do not pay the minimum amount due on the statement date, the bank levies a late payment charge. This is on top of the interest that has to be paid for the amount spent using the credit card.

The rate of late payment charge varies from bank to bank.

A credit score is a three digit number that represents the creditworthiness of a person. The number ranges from 300 to 900. A credit score of 750 or more is considered to be healthy and allows better borrowing terms like greater loan amount, lower interest rate, and longer tenure.

Using your credit card frequently and making timely repayment of the card’s dues is a way to improve your credit score. However, caution must be taken to not overspend and fall in a debt trap as it has a negative effect on the credit score.

Credit cards are not just a source of short term loans but also have various rewards and benefits to suit the different needs of various users. You can choose a suitable credit card based on your income (helps you decide the credit limit of your card), your requirements (which reward/cashback system works for you) and many more features.

Select has the Card Genie feature to help make this selection process much easier.

In case of loss or theft of credit card, users must immediately contact their bank/credit card provider to report said loss/theft and block the card.

This stops the card from being used without the owners authorisation and protects their funds.

Your credit card network decides whether it can be accepted for overseas transactions. Visa and Mastercard credit cards are usually accepted by most merchants globally. Overseas transactions do attract a “foreign currency markup” fee.

Contact your credit card provider to better understand the international application of your credit card.

A card network, or payment network, is a system that facilitates electronic transactions between a cardholder and a merchant. Examples include Visa, Mastercard, and American Express. These networks set standards, connect banks, and ensure secure and standardised processing of payments, enabling global and online commerce.

RuPay is a domestic payment network offered by banks and is accepted only in India. These cards have a lower processing fee and faster processing speed as compared to the other international services like Visa/MasterCard.

Yes, you can use your credit card abroad—provided the merchant accepts it. Visa and Mastercard are widely accepted internationally, so they usually work without issues. American Express and Discover also have a global presence but may not be accepted as commonly as the other two.

When you find out that your credit card has been lost or stolen, call your bank to report the loss. You can also block your card from your online banking app or via net banking. The bank will cancel the card and send you a new card with a new account number, expiration date, and security code.

Yes, banks usually charge a reward redemption fee of ?99. However, if you choose to redeem your reward points as cashback, this fee is not applicable. To redeem as cashback, you’ll need to have at least 2,500 reward points in your credit card account.

Add-on Credit Cards, are the ones that are issued against a primary credit card. They are a form of secondary or supplementary credit card. If you are a primary cardholder, you can apply for add-on cards for your children, spouse, or even your parents.

A foreign transaction fee is an amount that credit card companies charge their customers whenever a transaction is made with a foreign currency or perhaps, passes via any foreign bank. To process a foreign transaction, the card issuer charges a percentage of the total transaction amount, which is usually 3% or more.

Credit cards come with a variety of benefits that make them a useful financial tool, including:

Easy access to credit

EMI facility for big-ticket purchases

Helps build your credit score

Automatic expense tracking

Purchase protection

Incentives and offers such as cashback, discounts, and reward points

Flexible credit usage based on your spending needs

An expiration date on a credit card is simply the date on which the card itself will no longer work and must be replaced. When cards expire, companies often take the opportunity to send new cards with updated logos and designs.

The concierge services that come with a Credit Card take care of all the wants and needs of their premium customers which can range from booking tours and holiday packages to event planning and golf bookings!

It is an organisation that collects and researches individual credit information and sells it to creditors for a fee, so they can make decisions about extending credit or granting loans. TransUnion CIBIL, Experian, Equifax, and CRIF High Mark are the official credit bureaus.

A credit score is a number that represents a person's creditworthiness, based on their credit history, repayment behavior, and credit usage. It helps lenders assess how likely you are to repay borrowed money.

Here’s how credit scores are typically categorized:

300–499: Very Poor

500–599: Poor

580–669: Fair

670–739: Good

740–799: Very Good

800 and above: Excellent

A higher score increases your chances of loan or credit approval with better terms, while a lower score may limit your options.

If any of your personal information changes, you can ask the credit bureaus to change it accordingly.

Debit cards draw money directly from your bank account at the time of purchase, so there's no need for repayment later. Credit cards allow you to borrow funds up to a limit and repay them over time, with at least a minimum payment due each month. Charge cards, however, require you to pay the full balance in one go every month—no carryover allowed.

Contactless Payment allows customers to make payments, without using cash or swiping the card. The customers must 'Tap' or 'Wave' their card over a card reader to use this method. After that, the terminal will connect with the Bank Account and the payment will be made, quickly.

When a credit card is issued against an FD account, it is called an FD-backed credit card. The money in your FD account serves as the security deposit against which the card is issued. Customers who do not have a credit score can apply for an FD-backed credit card. Secured credit cards are a special type of card that requires a cash deposit — usually equal to your credit limit — to be made when you open the account. This money then acts as collateral every time you make a purchase.

A period usually between 20-25 days, during which the cardholder can pay the balance in full without incurring any interest charges. Every major credit card issuer gives you a grace period when you pay your statement balance in full by the due date. Federal law does not require a grace period, but when an issuer offers one, it must be at least 21 days. If your credit card carries a balance from the last billing cycle, there is zero chance of enjoying the leverage of the grace period as there is no credit card grace period after the due date.

No worries! Contact us and we'll resolve it right away!

Contact Us

30 stocks for the long term, investing concepts, premium valuation tools and much more await you with Finology Subscription!

Copyright © 2026 All rights reserved with Finology Ventures Pvt Ltd | All logos and Trademarks registered with their respective owners.

Privacy Policy Terms of use Refunds Policy